Companies that have financial expenses for fundamental or applied research and experimental development.

There are no sector or size restrictions

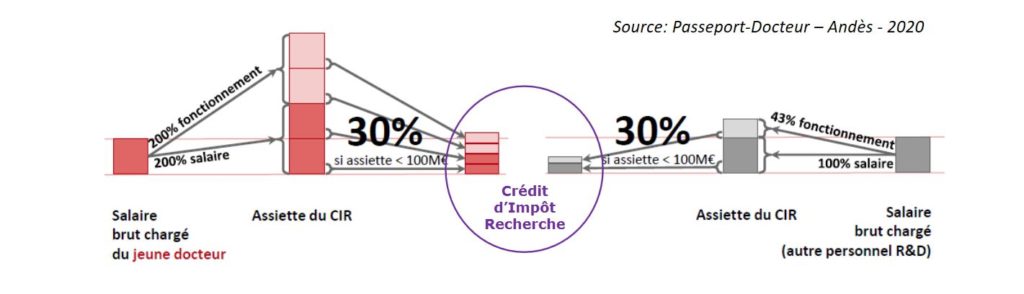

Which tax credit?

Eligible expenses = 100% of R&D personnel expenses + 43% of operating expenses related to these jobs

The rate varies according to the expenses incurred ➢ If annual expenditure <100 M€, CIR= 30% of eligible expenditure ➢ If expenditure >100 M€, CIR = 5% of eligible expenditure

The Young PhD scheme : an asset for PhDs to promote to companies

What is the Young PhD scheme?

It is a special case of the CIR which doubles the tax advantage for the company.

Its objective?

To encourage the employment of PhDs on permanent contracts by companies

How does it work?

Eligible staff expenses relating to PhDs hired for the first time on permanent contracts (salary + operating costs relating to these jobs) are taken into account for double their amount during the first 24 months.